02-Mar-2026 Provisional Refund under GST in case of taxpayers impacted by Inverted Duty Structure

#gstrefund #gstcouncil #gstreformsThe recent amendments brought in through GST 2.0 reforms (56th Council Meeting held in Sep-2025) have resulted into situations wherein the rates of taxes on various products (outputs) had been reduced without corresponding decrease in rate of tax on inputs. This has given rise to new categories of taxpayers who are getting impacted by the inverted duty structure. To mitigate the difficulties of such dealers, the GST law has been amended to extend the benefit of grant of provisional refund to such taxpayers. This will be a key liquidity booster for such select segment of taxpayers.

What is Inverted Duty Structure?

Inverted duty structure arises in cases where the rate of tax on inputs (eg 18%) is higher than the rate of tax on output( eg 5%).

What is Provisional Refund?

One of the most crucial pain points for certain businesses under the GST regime has been delays in refund processing, leading to substantial working capital blockage. To address this issue, the concept of provisional refund was introduced under the CGST Act, 2017.

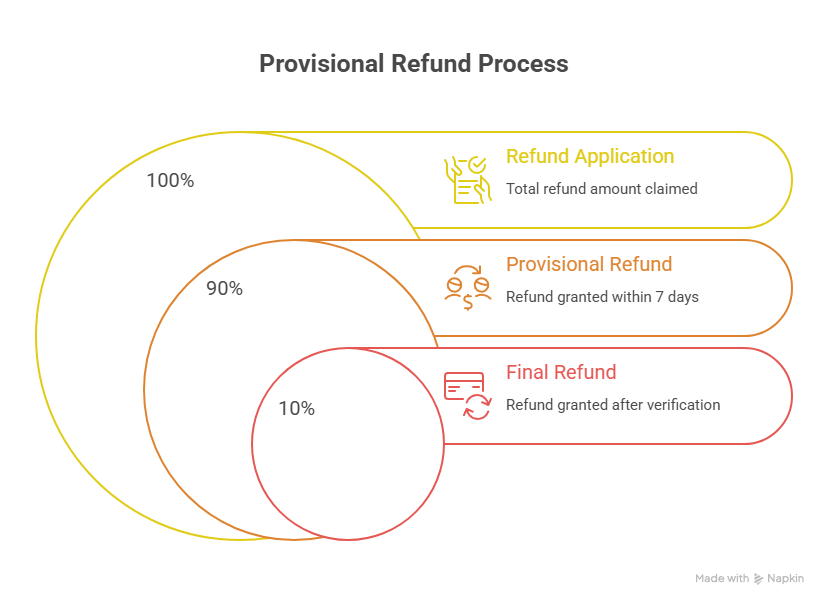

As per the existing provisions of GST law, in respect of refund claims on account of zero-rated supplies of goods or services or both (under LUT), the proper officer can sanction a provisional refund of up to 90 % of the total amount claimed (subject to prescribed conditions, limitations and safeguards), before the final settlement of the refund claim after due verification of documents.

Extension of Benefit of Provisional Refund

The benefit of grant of provisional refund has now been extended to include refunds arising out of inverted duty structure.

The proper officer can sanction a provisional refund of up to 90 % of the total amount claimed within 7 days of filing the refund application. However the provisional refund is not automatic or final—the balance 10% will be granted after due verification, safeguarding revenue interests. For the said verification and grant of final refund, the officer has timeline of 60 days from date of filing of refund application.

The provisional refund mechanism reflects taxpayer-centric approach. The proposed extension of this benefit to inverted duty structure cases is a welcome move that addresses long-standing liquidity concerns of businesses. The amendment will lead to improved cash flow for businesses stuck with accumulated ITC due to inverted duty structure. This reduces working capital blockage, which is a major concern in inverted duty cases.

Please feel free to reach out to us at info@apmh.in for any clarifications or further assistance.