02-Apr-2026 Intermediary Services : Game-Changing GST Amendment

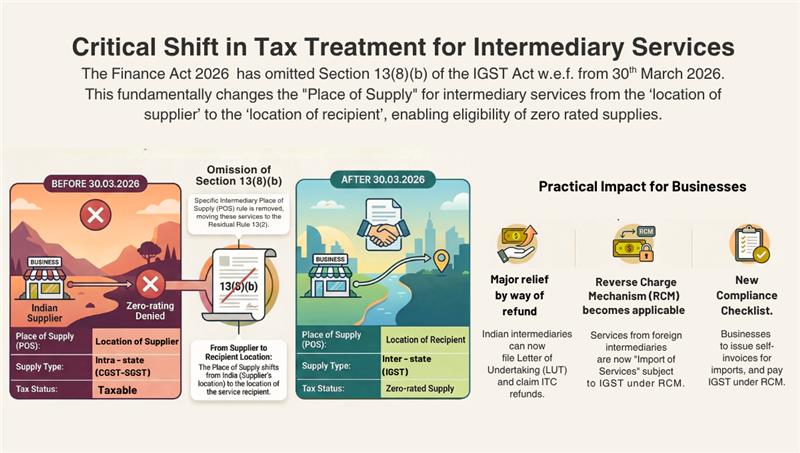

#intermediaryservices #placeofsupplyrules #igstact2017 #gstamendment2026 #commission #indentingcommissionThe Finance Act, 2026 has introduced a significant change to the Integrated Goods and Services Tax (IGST) Act, 2017, fundamentally altering how intermediary services are taxed in cross-border transactions. This amendment, effective through Clause 157 of the Finance Act, marks a shift towards a more equitable, destination-based taxation framework. The said amendment is brought in by way of omission of clause (b) in section 13(8) of the IGST Act and is operational from 30-03-2026 i.e. from the date of publication in Official Gazette of Finance Act 2026 pursuant to assent received from the President of India.

Understanding Intermediary Services: The Foundation

Before diving into the amendment, it's essential to understand what constitutes "intermediary services" under GST law.

According to Section 2(13) of the IGST Act, an intermediary is defined as a broker, an agent or any other person, by whatever name called, who arranges or facilitates the supply of goods or services or both, or securities, between two or more persons, but does not include a person who supplies such goods or services or both or securities on his own account.

The commission agents and indenting agents who receive commission from their foreign counterparts also qualify as intermediary, apart from other taxpayers who arrange and facilitate the supply.

What's Changing?

The Old Rule- (A Supplier-Centric Approach): Previously, Section 13(8)(b) of the IGST Act mandated that the place of supply for intermediary services was always the location of the supplier, regardless of where the recipient was located. This created a unique exception to the general principles governing service taxation.

The New Rule- (Substantial Revision): The amendment removes Section 13(8)(b) entirely. With this omission, intermediary services will now follow the default provisions under Section 13(2) of the IGST Act. Under this section, the place of supply is determined as:

This is a complete reversal from the earlier position where the supplier's location was the determining factor regardless of recipient location.

Why This Matters: The Export Opportunity

This seemingly technical change has profound practical implications for Indian intermediaries serving foreign clients.

Qualifying for Export of Services

When an Indian intermediary provides services to a recipient located outside India, the place of supply now shifts outside India. This is crucial because it satisfies one of the key conditions required for classification as "export of services" under Section 2(6) of the IGST Act.

To qualify as export of services, all the following conditions must be met:

- 1. The supplier must be located in India

- 2. The recipient must be located outside India

- 3. The place of supply must be outside India (now possible due to this amendment)

- 4. Consideration must be received in convertible foreign exchange

- 5. The supplier and recipient must not be merely different establishments of the same legal entity

Indian intermediaries can now avail zero-rated supplies, claim refunds of input tax credit, and compete more effectively in international markets. Such taxpayers should apply for Letter of Undertaking (LUT) before issuing the Export invoice as per the amended provision to avail the benefit of Export of Services without payment of tax.

End of Long-Standing Controversies: A Major Relief

The Litigation Landscape Under Old Law

The special place of supply rule for intermediary services under Section 13(8)(b) has been a major source of litigation and disputes since GST implementation in 2017. The controversies primarily centred around two key areas:

- 1. Classification Disputes: What Qualifies as "Intermediary Service"? - Tax authorities and taxpayers frequently disagreed on whether a particular service qualified as intermediary service or should be treated as a principal-to-principal supply.

2. Place of Supply Determination Controversies - Even when a service was accepted as intermediary service, disputes arose regarding the application of Section 13(8)(b).

Now, after the amendment: With the removal of Section 13(8)(b), intermediary services are no longer a "special category" with unique place of supply rules. The place of supply treatment is uniform i.e. recipient location applies whether it's intermediary service or regular service and even if reclassified, place of supply treatment remains the same (recipient location)

Alignment with GST Principles

This amendment represents more than just a procedural change. It brings intermediary services in line with the destination-based taxation principle that forms the foundation of GST. By removing what was essentially an artificial deeming provision, the government has created parity between intermediary services and other cross-border service transactions.

The destination principle ensures that tax is levied where the consumption occurs, a globally recognized standard for indirect taxation.

The Reverse Impact: Import of Services

The amendment works both ways. When a foreign intermediary provides services to an Indian recipient, the transaction will now be classified as import of services. In such cases, the Indian recipient will be liable to pay GST under the Reverse Charge Mechanism (RCM).

This creates symmetry in the tax treatment and ensures that the Indian tax base is protected while simultaneously providing export benefits to domestic service providers.

Conclusion: A Transformative Reform Ending Years of Uncertainty

The amendment to Section 13 of the IGST Act represents a significant step toward rationalizing India's GST framework for cross-border intermediary services. By eliminating the supplier-location rule for intermediary services and adopting the destination principle, this change creates a level playing field for Indian intermediaries in the global marketplace while ending years of costly litigation and business uncertainty.

Businesses must review contracts, update compliance systems, train teams, and implement robust documentation processes. Those who act swiftly will gain first-mover advantages in newly accessible export markets, while those who delay risk non-compliance penalties and missed opportunities.