When a Valid VAT Claim Can Still Change Later?

A business can claim input VAT correctly on a capital asset and still face a reversal years later if the asset's actual use changes over time. In one common audit scenario, a business walks into a ZATCA review confident its VAT position is clean, only to discover that a building, system, or machine claimed years ago should have been adjusted because its taxable use changed during the review period. That kind of surprise does not happen because the original VAT claim was wrong. It happens because the business treated capital asset VAT as a one-time exercise instead of an annual control process.If you are a finance head, tax manager, or business owner in KSA, this issue matters more than it may first appear. Capital asset VAT adjustments directly affect cash flow, audit exposure, and the accuracy of your VAT recovery.

Many businesses correctly recover input VAT when purchasing capital assets. However, VAT recovery does not always end with the initial claim. If the actual use of the asset changes over time, the input VAT originally recovered may need to be adjusted.

This is one of the most overlooked areas of VAT compliance. Businesses often focus only on the purchase-stage recovery and fail to monitor how the asset is actually used during subsequent years. As a result, businesses may either lose legitimate VAT recovery opportunities or face compliance exposure during VAT audits.

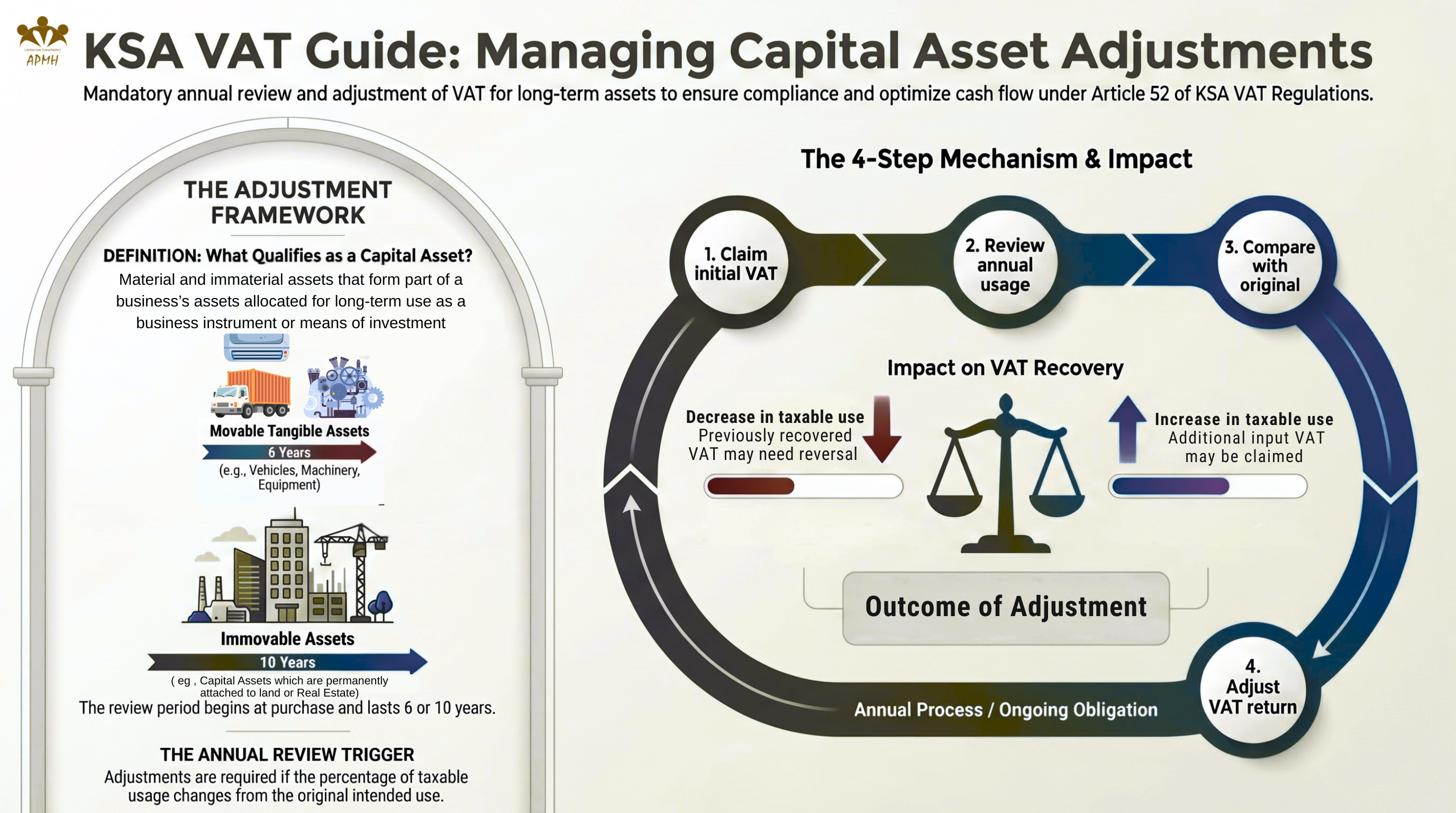

Under Article 52 of the VAT Implementing Regulations, taxable persons are required to review the use of capital assets throughout the adjustment period and revise input VAT recovery wherever necessary.

Who Should Review Capital Asset Adjustments?

This topic is especially relevant if you are managing VAT for a business that owns long-term operational assets in KSA. Capital asset adjustment provisions are particularly relevant for businesses owning assets.

These rules become especially important where businesses:

- Change from taxable use to mixed use

- Increase in exempt activities

- Transfer of assets to non-business use

- Sale of capital assets during adjustment period

- Permanent disposal or withdrawal of assets

- Change in business model or operational structure

Understanding the Capital Asset Adjustment Mechanism

The adjustment mechanism works through a periodic review process.

Step 1 — Initial Input VAT Recovery

At the time of purchase, the business claims input VAT based on the intended taxable use of the asset.

Step 2 — Annual Usage Review

At the end of each twelve-month period, the business reviews the actual taxable use of the asset.

Step 3 — Comparison of Usage

The actual taxable usage is compared with the original intended taxable usage.

Step 4 — VAT Adjustment

Any increase or decrease in taxable usage results in an adjustment in the VAT return for the last tax period falling within that twelve-month period.

| Scenario | VAT Impact |

|---|---|

| Increase in taxable use | Additional input VAT may be claimed |

| Decrease in taxable use | Previously recovered VAT may need reversal |

Adjustment Period for Capital Assets

The adjustment period depends upon the nature of the capital asset.

| Asset Type | Adjustment Period |

|---|---|

| Movable assets | 6 years |

| Immovable capital assets | 10 years |

The adjustment period begins from the date of purchase. If the accounting useful life is shorter, the shorter period applies.

APMH Perspective

Capital asset adjustment is one of the most practical VAT control mechanisms available to businesses.

The stronger view is this: businesses treating capital asset VAT as a one-time exercise are not just creating compliance risk, they are often mismanaging working capital. In practice, this area is ignored because the rules are difficult to understand. It is ignored because no one has built a simple annual review habit around asset usage, and that gap can become expensive.

Businesses are advised to manage this area effectively — treat VAT on capital assets as an annual decision-making process rather than a one-time accounting entry.

Please refer to the full version with practical examples.

↓ Download PDF